3 Key Reasons Coupang Now Appears Compelling

RUNSTUDIO

Introduction

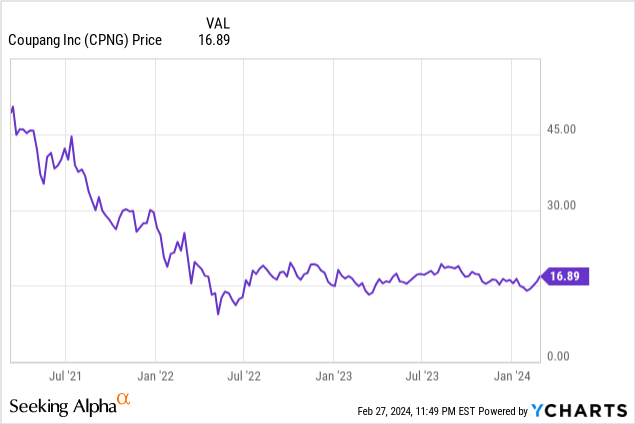

Coupang (NYSE:CPNG) is a Korean-based online retailer. Often dubbed the “Amazon of Korea”, the company IPO’d on the New York Stock Exchange back in March 2021 and opened in the mid $50s per share. Unfortunately, the stock sold off over the next year, before bottoming out at around $9 per share in April 2022. Since then, the stock has rebounded, but has mostly traded range-bound between $13 and $20 per share.

That might be about to change after the company reported 2023 Q4 and FY results on February 27. Here are three reasons Coupang now may appear compelling.

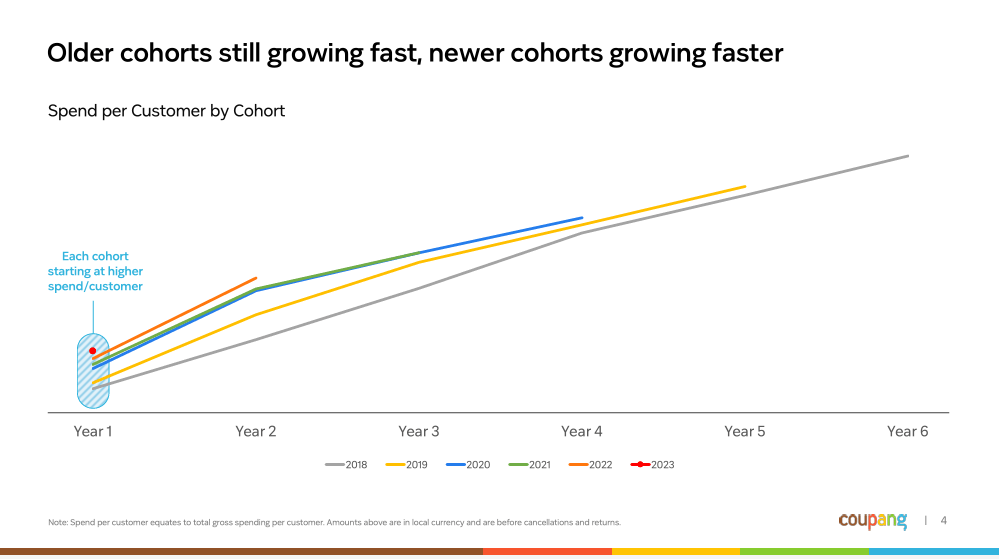

Reason #1: Accelerating Non-Financial KPIs

Coupang highlights several metrics in their investor presentations that serve as good Key Performance Indicators for investors. In their most recent Q4, report, virtually all of these saw solid increases both Quarter-over-Quarter and Year-over-Year. Readers can refer to the presentation found on their investor relations page here.

The first KPI in the presentation highlights Spend Per Customer by Cohort. This saw a boost in 2020 as consumers turned to online commerce during the COVID-19 pandemic. It then stalled in 2021 before picking back up in 2022. Now, 2023 continues the trend, with the current new Customer Cohort spending more than in previous years. It appears this trend will remain solid going forward.

Customer Spend by Cohort (Coupang Q4 and FY 2023 Investor Presentation)

Active Customers increased from 18M in Q4 2022 to 21M in Q4 2023, up 16% YoY and up steadily every quarter in 2023.

WOW members, which is essentially Coupang’s version of Amazon Prime, increased even faster than Active Customers. WOW members increased from 11M at the end of 2022 to 14M at the end of 2023. This is a subscription offering costing just 4990 won (About $3.75 USD) monthly. Subscribers receive access to free shipping, special offers, video streaming services, and more. I believe that Coupang will eventually have pricing power with this service, but their current strategy to keep the price low to onboard new customers rapidly is likely the correct strategy for now.

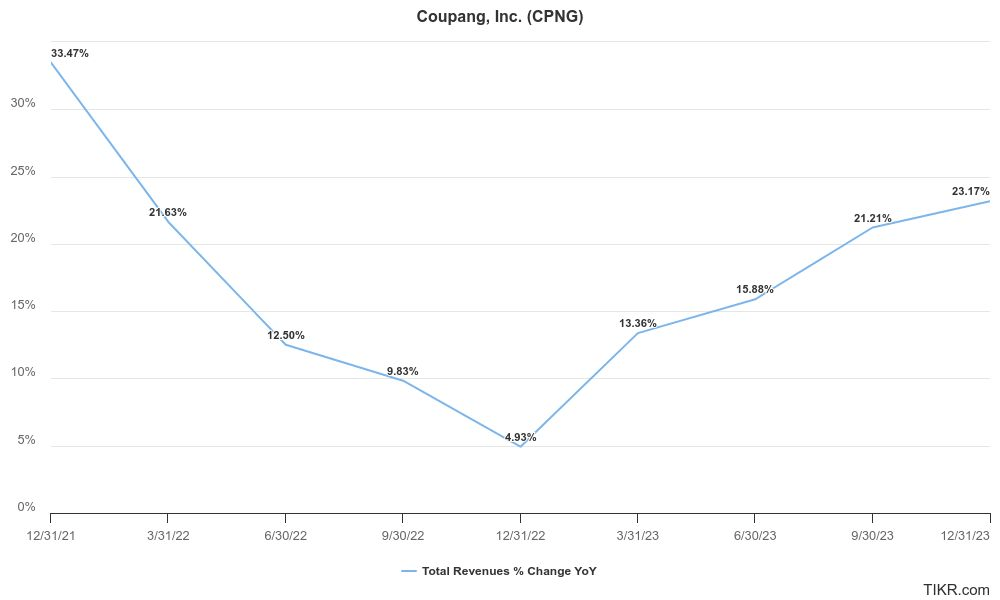

Reason #2: Accelerating Revenue and Operating Leverage

Revenue growth accelerated in both Q4 and the entire 2023 year over the same periods in 2022. Total revenue growth in 2022 was 11.8%. In 2023, that accelerated to 18.5% total revenue growth YoY. The quarterly revenue numbers show a similar story, with revenue accelerating quarter-over-quarter in four straight quarters. If this momentum continues in 2024, then revenue growth could have yet another strong year.

Coupang Revenue % Change YoY (TIKR.com)

This accelerating revenue growth has led to significant operating leverage. Operating income grew 57% YoY in Q4, and operating income for the full year was a positive $473M for the first time ever, up substantially from the $112M loss the company posted in 2022.

Net income grew as well, but the company benefitted from an $895M tax-related reserve gain that showed up on the bottom line. If you take this one-time gain out, the company earned adjusted net income of $465M, and adjusted diluted EPS of $0.26 for the full year.

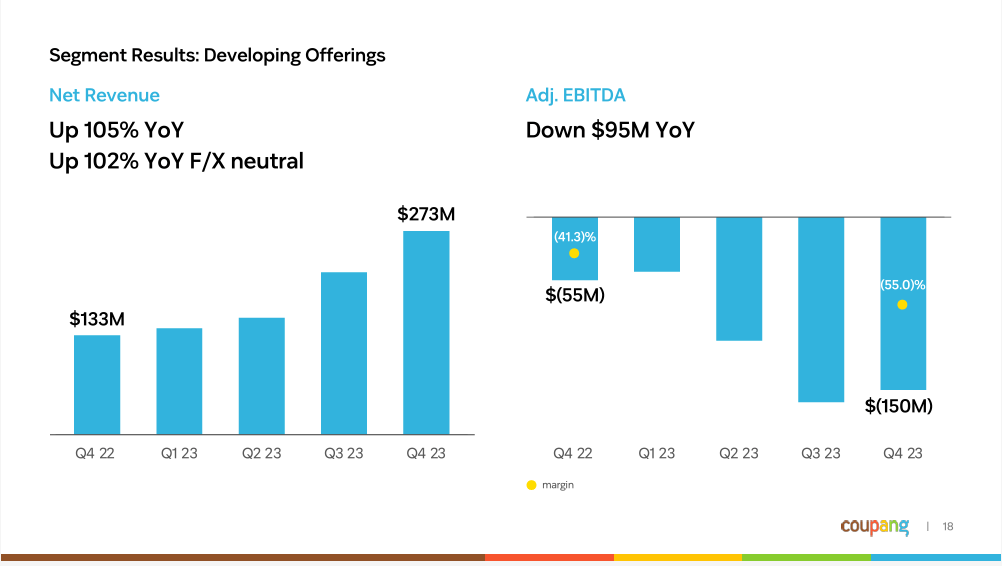

Reason #3: Extreme Growth in Developing Offerings Segment

Coupang’s Developing Offerings segment includes international operations, as well as Coupang Eats, Coupang Play and Fintech services.

Q4 saw the Developing Offerings segment grow revenue to $273M from $133M in Q4 of 2022. This was good for 105% growth YoY, and one can clearly see how this segment began to accelerate beginning in Q3 2022 in the company’s earnings presentation.

Developing Offerings Revenue (Coupang Q4 and FY 2023 Investor Presentation)

Perhaps unsurprisingly, this segment still loses a substantial amount of money, posting adj. EBITDA of negative $150M in Q4. This, however, is a leveling off from Q3. It remains to be seen what this segment does going forward, however, I’d expect it to reach a critical point where losses begin to decrease as revenue grows rapidly and eventually reaches break even sometime in the next few years.

Valuation

Coupang’s margins are still razor-thin. This means assessing valuation is difficult, as it’s unclear what margins might be at maturity.

Coupang currently trades right around 1X sales. In the past, it’s traded as high as 5X sales, but I doubt we’ll see that multiple again anytime soon, if ever. At 1X sales, there is certainly room for multiple expansion if the company can continue to demonstrate an ability to leverage fixed costs into higher earnings.

Coupang’s operating margin came in at 1.9% in 2023, or $473M. The stock has a market cap of $30B and an enterprise value of $27.8B. This means that despite the low sales multiple, the stock trades at a little over 60 times operating income, which makes the stock appear more expensive. However, I’d point out that if margins merely increase to 3% through operating leverage, operating income would jump by over 50%. Combine that with the company’s numerous opportunities for further revenue growth, and there remains significant potential for Coupang to continue growing earnings very quickly in the future, and thus I don’t believe current earnings are a great way to value the business.

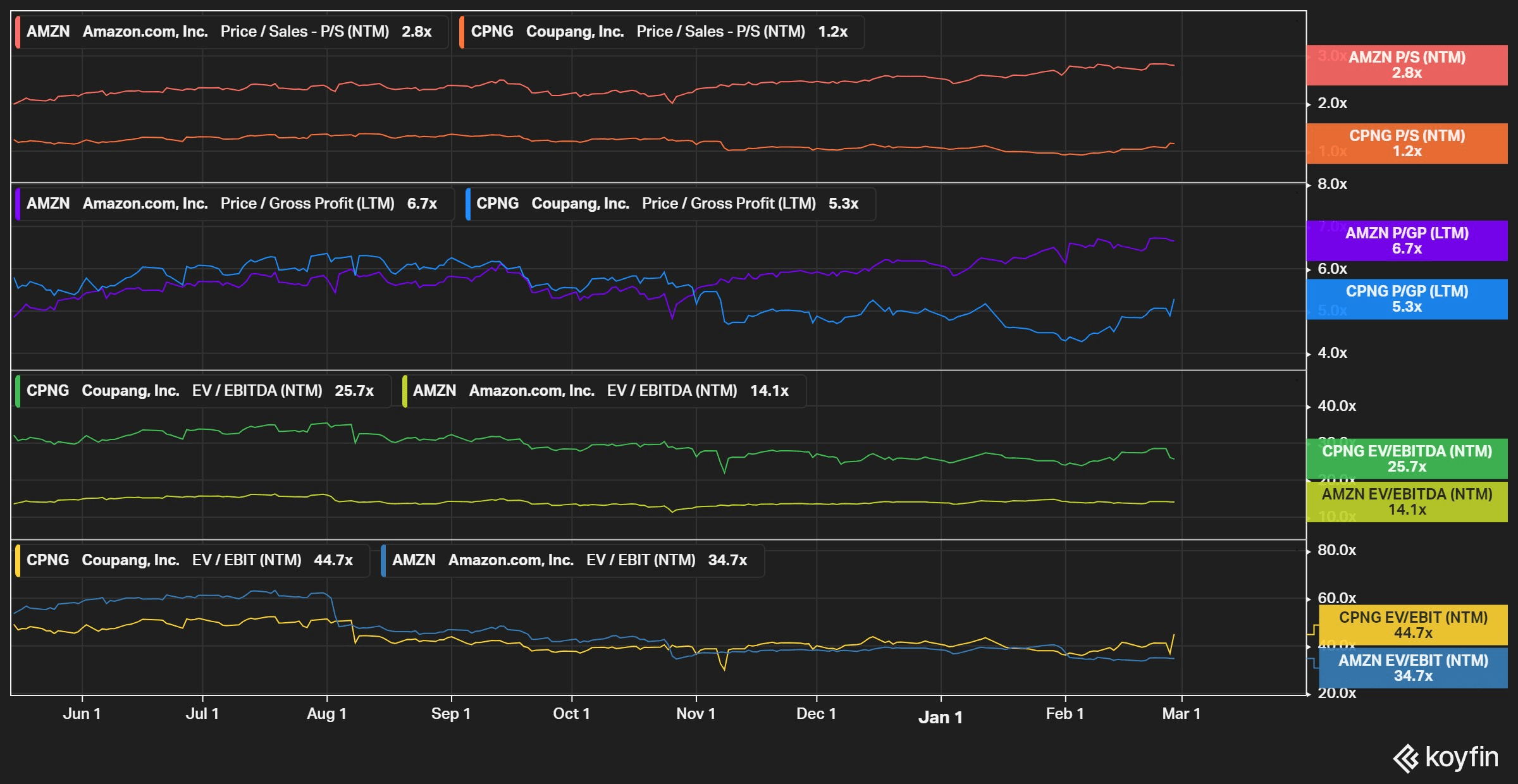

Depending on which NTM multiple you want to choose, Coupang either trades favorably or unfavorably against Amazon. However, this is far from a perfect solution due to Amazon’s AWS segment accounting for a large portion of its valuation.

CPNG vs AMZN Multiples (Koyfin.com)

Potential Risks

I consider the following to be the key risks to an investment in Coupang:

- Competition:

- Amazon has a limited presence in South Korea. Items ordered on Amazon in Korea often have long shipping times. However, if Amazon decided to invest in the country, they could bring significant resources in quickly.

- This is mitigated by Coupang’s strong existing brand and infrastructure that allows for same-day delivery. Amazon does not have this capability in Korea currently.

- Alibaba (BABA), eBay (EBAY), and Carousell are other competitors that should be monitored.

- Amazon has a limited presence in South Korea. Items ordered on Amazon in Korea often have long shipping times. However, if Amazon decided to invest in the country, they could bring significant resources in quickly.

- Korean Demographics

- Korea has recently experienced very low birth rates, with some now predicting a population decline later this century. This could lead to low long-term growth rates in GDP for Korea, and thus Coupang as well.

- Asian Geopolitical Concerns

- South Korea and North Korea have peacefully co-existed for decades now. However, if one provokes the other, the possibility of a war breaking out should be considered. This would very likely impact Coupang’s operations in South Korea severely.

- Coupang recently entered Taiwan. Taiwan has been the subject of debate around what China’s ultimate plans are for the territory. A potential Chinese invasion of Taiwan could severely impact Coupang’s operations in Taiwan.

Conclusion

Coupang’s metrics are all trending in the right direction. I expect this is likely to continue in 2024, though we may see revenue growth rates slow a bit rather than accelerate going forward, especially in the second half of 2024 when the company will face tough YoY comps. Nonetheless, on a sales multiple basis, the valuation is not particularly demanding, and I could see Coupang doing well from here going forward.

Original Source